Who Is Driving Microsoft's Record Cloud and AI Revenue, and What Do the Q3 2026 Numbers Actually Mean?

Microsoft has delivered one of the clearest signals yet that enterprise demand for cloud computing and artificial intelligence is not slowing down, even as macroeconomic volatility and geopolitical uncertainty weigh on corporate spending decisions globally. The company's fiscal third quarter results for 2026 exceeded analyst expectations across every headline metric, and the numbers behind the headline deserve careful reading.

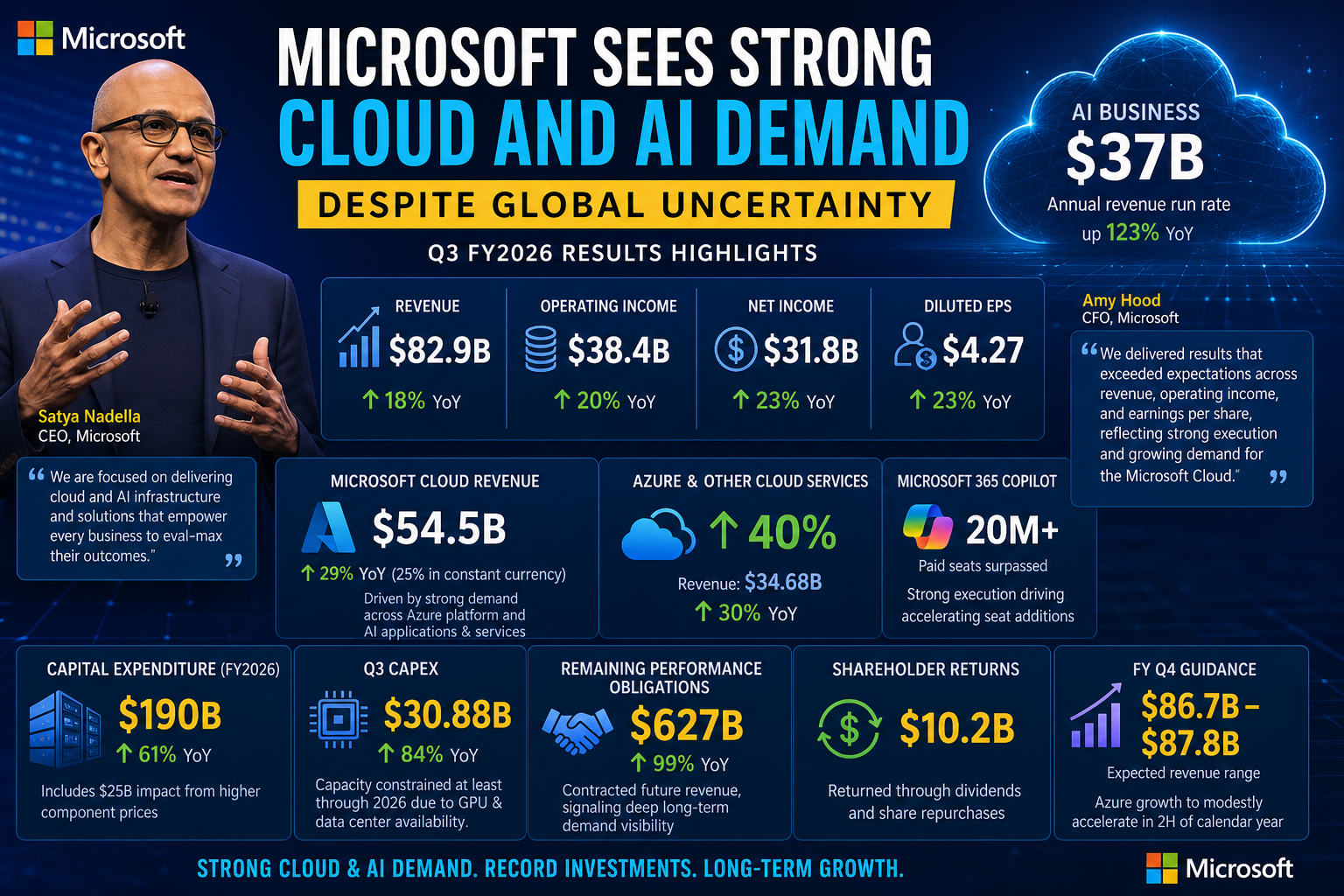

Revenue for the quarter ended March 31, 2026, reached $82.9 billion, an increase of 18% year over year. Operating income came in at $38.4 billion, up 20%, while net income rose 23% to $31.8 billion. Diluted earnings per share reached $4.27, also up 23%.

For an economy correspondent tracking where institutional capital is actually flowing in 2026, these numbers represent something more than a strong quarter. They confirm that AI infrastructure spending has moved from discretionary to essential in corporate budget planning.

Who Said What: Satya Nadella and Amy Hood on Cloud and AI Momentum

Who speaks from the Microsoft earnings podium shapes how markets interpret the results, and both the CEO and CFO delivered statements that carry significant forward-looking weight.

CEO Satya Nadella framed the quarter around the agentic computing era, saying: "We are focused on delivering cloud and AI infrastructure and solutions that empower every business to eval-max their outcomes."

Nadella's most striking disclosure was about the speed of AI revenue growth. Microsoft's AI business surpassed an annual revenue run rate of $37 billion, up 123% year over year. That figure, more than doubling in a single year, places Microsoft's AI business alone among the largest software franchises ever built.

CFO Amy Hood anchored the quarter's credibility with a summary that left little room for interpretation. Hood said the company "delivered results that exceeded expectations across revenue, operating income, and earnings per share, reflecting strong execution and growing demand for the Microsoft Cloud."

Who Is Buying Microsoft Cloud and How Fast Is Azure Growing?

Understanding who is purchasing Microsoft's cloud services matters for assessing whether this growth is broad-based or concentrated in a narrow segment of large enterprise clients.

Microsoft Cloud revenue was $54.5 billion, growing 29% and 25% in constant currency, reflecting strong demand across the Azure platform and first-party AI applications and services. Results were ahead of expectations, as Microsoft delivered capacity earlier in the quarter, enabling increased consumption across both AI and non-AI services.

Azure, the core engine of that cloud segment, continued its acceleration. Growth of 40% in Azure and other cloud services cleared the roughly 39% analysts had penciled in. Revenue for the wider Intelligent Cloud segment, covering Azure, server products, and the GitHub and Nuance cloud services, came in at $34.68 billion, a 30% increase from a year ago.

Strong customer demand across workloads, customer segments, and geographic regions continues to exceed available capacity. That last phrase is the critical one from a macroeconomic standpoint: supply, not demand, is the binding constraint on Microsoft's cloud growth trajectory heading into the second half of 2026.

Who Is Using Microsoft's AI Products and What Is Copilot's Market Penetration?

The commercial adoption of generative AI tools has been a contested question across the technology sector since the initial wave of product launches. Microsoft's Q3 data provides one of the most concrete measures of real enterprise uptake available.

Microsoft 365 Copilot paid seats surpassed 20 million, with strong execution and improving product quality driving accelerating seat additions during the quarter.

Microsoft is also shifting its commercial model in ways that will compound revenue beyond seat counts alone. CEO Nadella told analysts: "Any per-user business of ours, whether it's productivity, coding, security, will become a per-user and usage business." That means customers will pay not only for access but for the volume of AI agent activity they consume, a structural pricing shift with significant long-term revenue implications.

Microsoft already is seeing 60% of its customer service customers in the business-app segment purchasing usage-based credits. GitHub Copilot is also moving to usage-based pricing as of June 1, and the Agent 365 control plane is set to become generally available on May 1.

Who Is Paying for Microsoft's Infrastructure Buildout and What Does the $190 Billion Capex Signal?

The capital expenditure story is where this earnings report carries its most consequential economic signal, both for Microsoft shareholders and for the broader technology supply chain.

In forecasting $190 billion in capital expenditure for calendar year 2026, which would be up 61% from 2025, CFO Amy Hood said she anticipates a $25 billion impact from higher component prices. The Visible Alpha consensus had estimated capex of $154.6 billion, meaning Microsoft's actual guidance came in roughly $35 billion above what Wall Street had modeled.

Microsoft's capex for the quarter jumped to $30.88 billion, up 84% year over year. For context, that single quarter's infrastructure spend exceeds the annual revenues of many Fortune 500 companies.

Hood said Microsoft expects to remain capacity constrained "at least through 2026." That constraint is being driven by GPU and data center availability, not by demand softness, which is an important distinction for anyone reading this as a sign of caution rather than confidence.

Hood stated that Microsoft is confident in managing physical component constraints and is focused on bringing more capacity online. The capex increase is driven by demand signals and involves both short-term assets like CPUs and GPUs and long-term investments.

Who Owns the Long-Term Revenue Backlog and What Does $627 Billion in Remaining Obligations Mean?

One figure in the Q3 results deserves particular attention for what it says about the durability of Microsoft's revenue base.

Commercial remaining performance obligations increased 99% to $627 billion. This represents contracted future revenue that customers have already committed to pay, the largest such figure Microsoft has ever reported and a near doubling in a single year.

Commercial remaining performance obligations standing at $627 billion, up 99%, signal deep long-term demand visibility. For investors and policy analysts watching whether AI investment is speculative or contracted, this backlog is meaningful evidence that large enterprises have locked in multi-year cloud and AI spending with Microsoft specifically.

Who Is Watching the Headcount and What Did Microsoft Signal About Its Workforce?

Microsoft's headcount will go down year over year in the 2027 calendar year, which will end in June 2027. "We continue to evolve how we operate, to increase our pace and agility," Hood said. The combination of rising AI productivity and workforce reduction is a pattern that will become increasingly visible across large technology companies throughout 2026 and 2027.

Who Returned Capital to Shareholders and What Did Microsoft Pay Out?

Microsoft returned $10.2 billion to shareholders through dividends and share repurchases during the quarter. That figure, delivered alongside a record capital expenditure program, reflects the financial headroom that sustained cloud and AI growth has created for the company.

Who Provided the Q4 Revenue Guidance and What Does the Outlook Say?

Microsoft's CFO Amy Hood called for $86.7 billion to $87.8 billion in fiscal fourth-quarter revenue, which represents continued sequential growth and would mark another record quarter if achieved. The guidance came in slightly below some analyst targets, which contributed to a modest dip in the stock price following the earnings release despite the strong headline numbers.

Despite capacity constraints and the continued need to balance incoming supply, Microsoft expects Azure growth to show modest acceleration in the second half of the calendar year compared with the first half.