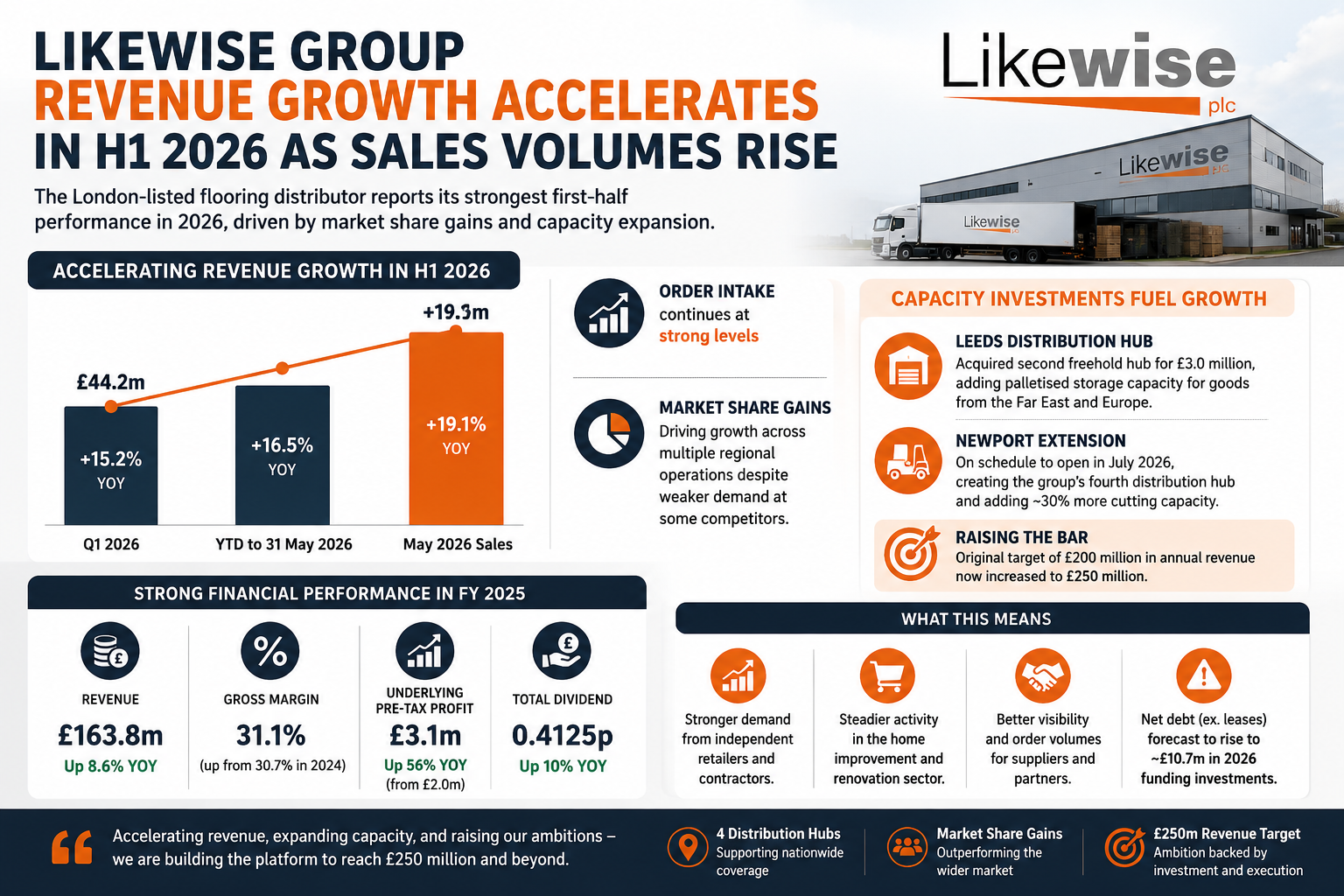

Likewise Group plc, the London-listed flooring distributor, has reported accelerating revenue growth through the first half of 2026, with trading updates pointing to its strongest run since listing. Total group revenue rose 15.2% to £44.2 million in the first quarter, then climbed further to 16.5% on a year-to-date basis through 31 May, with sales in May alone up 19.1% against the same month last year. Formal audited interim results for the six months to 30 June are due later in the year, but the company's own trading statements already show a clear acceleration as the half progressed.

A First Half Built on Accelerating Momentum

The pattern across 2026 is unusual for a sector where Q1 is typically the quietest stretch of the year. Instead of fading after a strong start, Likewise's growth rate has widened:

- Q1 2026 revenue: up 15.2% to £44.2 million.

- Year-to-date revenue to 31 May: up 16.5%.

- May 2026 sales alone: up 19.1% year on year.

- Order intake described by management as continuing at strong levels.

That progression matters because it suggests the growth is not a one-off comparison effect. Q1 2025 itself had already grown 10.7% against Q1 2024, so this year's gains are being layered on top of a relatively strong prior period rather than a soft one.

Where the Growth Is Coming From

Management has pointed to market share gains as the main driver, particularly notable given that several UK competitors have recently flagged weaker demand. Likewise operates across multiple regional units, including Likewise Floors, Valley Wholesale Carpets, and its Manchester and Birmingham operations, giving it a broader footprint to capture business as smaller rivals struggle.

Capacity Investment Underpins the Growth Story

Revenue growth at this pace only holds up if a distributor can actually move the product, and Likewise has been spending accordingly. The group acquired a second freehold distribution hub in Leeds for £3.0 million earlier this year, adding palletised storage capacity for goods arriving from the Far East and Europe. A separate extension at its Newport site remains on schedule to become operational in July 2026, creating what will be the group's fourth distribution hub for Likewise Floors and adding roughly 30% more cutting capacity.

Together, these projects are designed to support a sales target that has effectively shifted twice in two years. The group's original goal of surpassing £200 million in annual revenue has already given way to internal commentary about pushing toward £250 million, a sign that management's confidence has outpaced its own prior planning.

From £200 Million to £250 Million Ambition

The scale-up is grounded in results already on the books. For the year ended 31 December 2025, Likewise reported:

- Total group revenue of £163.8 million, up 8.6% year on year.

- Gross margin improvement to 31.1%, from 30.7% in 2024.

- Underlying pre-tax profit up 56% to £3.1 million, from £2.0 million.

- A 10% increase in total dividend for the year, to 0.4125p per share.

Those figures show a business that grew revenue at a high single-digit pace last year while improving profitability faster than sales, which is part of why the acceleration into double-digit growth this year has drawn attention from analysts who had penciled in more modest expansion for 2026.

What This Means Beyond the Balance Sheet

A flooring distributor's order book is a reasonable proxy for activity further down the construction and home renovation chain. Rising sales volumes at Likewise point to steadier demand among independent flooring retailers and contractors, even as broader UK consumer spending data has looked uneven this year. For suppliers, faster throughput at an expanding distributor means more predictable order volumes. For the wider sector, a distributor gaining share while its capacity expands is one of the clearer signs that demand for home improvement and renovation work has not slowed as much as headline retail figures might suggest.

The risk sits on the other side of the balance sheet. Net debt excluding lease liabilities is forecast to rise to around £10.7 million for 2026 as the group funds its property purchases, a manageable level against current cash generation but one worth watching if growth slows before the capacity investments are fully utilised.